Question of the day

What are the fiscal policy measures for 2021?

Income tax

Exemptions for natural persons

In order to mitigate the impact of inflation on citizens’ incomes, as well as to support families with children, it is proposed to:

· increase the personal exemption and the major additional exemption by 5 % – from RON 24 000 to RON 25 200 and from RON 18 000 to RON 18 900 respectively

· increase the exemption for persons maintained by 50 % – from RON 3 000 to RON 4 500.

By increasing the personal exemption, citizens will pay RON 144 less income tax, i.e. the salary will also be increased by the same amount. Citizens who benefit from the exemption for persons maintained will pay RON 180 less income tax, while their income will be increased by RON 180.

In order to simplify the mechanism for taxing natural persons and to encourage all persons to take up employment, it is proposed that the exemptions granted to spouses in the size of RON 11 280 be abolished, while retaining the major additional exemption. In this way, citizens who have benefited from this exemption will pay a tax higher, in the amount of RON 1353,6.

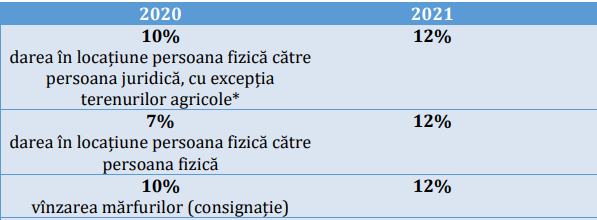

Uniform income tax rates

In order to simplify the tax administration process, both at the level of the tax authority and at the level of the taxpayer through the absence of the obligation to submit a tax return, measures are proposed to standardise income tax rates.

Thus, in order to achieve the objectives set, it is proposed to align the income tax rates at the level of the general rate of 12 %.

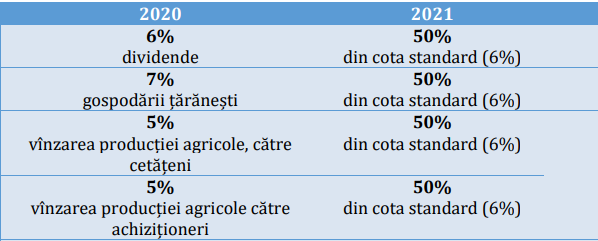

At the same time, in order to ensure the investment attractiveness of the national economy, the tax rate on dividend income is proposed to be maintained at the level of 6 %, which will represent 50 % of the standard rate. Similarly, 50 % of the standard rate (6 %) is to be taxed on income earned by individuals and purchases from the sale of agricultural production.

Taxation of income financial

In accordance with Article 24 (7) of the Law implementing Titles I and II of the Fiscal Code No nr.1164/1997, the interest of resident natural persons, with the exception of those registered in a legal form of business organisation, from bank deposits shall not be taxed until 1 January 2021; corporate securities in the form of bonds and transferable securities, including money market instruments such as bank certificates of deposit and bank bills of exchange; members’ deposits on personal savings accounts in savings and loan associations of citizens located in the territory of the Republic of Moldova.

With this project, it is proposed to tax interest from deposits at the rate of 3 % (25 % of the standard rate) through the final withholding of income tax, which will ensure simplicity in the process of tax administration.

Abolition of taxation of dividends distributed to legal persons

To ensure that tax law does not provide for taxation of the same income with the same tax it is proposed that the 6 % withholding tax on dividends should only apply to distributions of dividends to individuals or non-residents.

Source: contabilsef.md