Question of the day

What do you do with 2 % of your income tax in 2021?

The percentage designation (the so-called “2 %” law) has been promoted in the Republic of Moldova for almost 20 years, largely by civil society. In 2013, for the first time, the Fiscal Code was amended to regulate this mechanism. Due to the amendment of the legislation, without complying with the provisions of the Constitution, the amendment of the Fiscal Code to establish the percentage designation was declared unconstitutional. Only in Moldova since 2017 can citizens, foreigners and stateless persons redirect 2 % of their annual income tax to a non-governmental organisation or religious entity. So far, legal persons cannot redirect 2 % to Moldova, although in many countries this is possible and even encouraged.

Percentage designation not a donation private or an act of philanthropy. It is an individual mechanism that is based on the responsible understanding that members of local society/communities support initiatives of social importance by allocating a percentage of the annual income tax paid. Thus, the tax payer delegates to the State his ‘desire’ to support public organisations or religious entities, typically for initiatives that the State fails to do. Individuals can therefore support activities at national, district or even village level in the fields of culture, social cohesion, animal protection, democracy and justice, human rights, social support, economic development, charity, environmental protection, sport, education, etc.

According to Article 152 of the Fiscal Code, natural persons who are entitled to redirect 2 % must pay income tax annually, not have income tax debts for previous tax periods (the debt can be verified here https://mpay.gov.md/) and complete the income statement. A person can only re-direct 2 % to a single beneficiary on an annual basis. If more than one beneficiary is indicated, this re-routing will be cancelled and the designated money will be transferred to the state budget.

Beneficiaries of designation percentages can be found on the list of beneficiaries drawn up annually by the Public Services Agency and published online. (list for 2021). Compliant Government Decision no 8 of 18.1.2019, beneficiary organisations included in the List of Beneficiaries in previous years are automatically registered in the List of Beneficiaries for the following year, provided that they do not have debts to the national public budget for previous tax periods. The list includes:

— obscure associations, foundations and private institutions registered in the Republic of Moldova carrying out activities of public utility provided that they operate for at least 1 year until registration in the list of beneficiaries is requested and do not have debts to the national public budget for previous tax periods;

— religious denominations and their component parts registered in the Republic of Moldova and carrying out social, moral, cultural or charity activities, provided that they carry out their activity for at least 1 year until they apply for registration in the list of beneficiaries and do not have debts to the national public budget for previous tax periods.

Public utility, as a condition for trade associations, foundations and private institutions, is regulated by

Law No 89 on non-commercial organisations. It is carried out in the general interest or in the interest of local authorities, and the exhaustive list is laid down in Article 21 of the same law. The certification committee shall award the status of public utility in accordance with the procedure laid down in Article 22 of Law No 89. Of the other part,

Law No 125 on freedom of conscience, thought and religion does not regulate any procedure for the certification or clarification of the social, moral, cultural or charity activities to be carried out by religious denominations and their constituent parts in order to be included in the List of Beneficiaries of Percentage Designation.

You can redirect 2 % only in person – by filling in the form CET18 physically or by submitting the income tax return electronically. The deadline in 2021 is 30 April. You must know the beneficiary’s tax code, displayed on the List of Beneficiaries, to be indicated in the income tax return.

According to point 20 of the Regulation on percentage designation mechanismThe State Tax Service does not validate the percentage designation when:

1) the individual’s income tax return for the tax period was submitted after the deadline;

2) the beneficiary of the percentage designation is not included in the updated List of Beneficiaries;

3) the individual taxpayer has income tax liabilities for periods prior to the tax period in which the percentage designation was made;

4) the taxpayer who is a natural person has not paid tax on the declared income from which the percentage designation was made;

5) the individual taxpayer indicated several beneficiaries in the individual’s income tax return for the tax period.

The beneficiaries of the percentage designation may request information from the State Tax Service on the number of persons and the place of origin of the natural persons who directed the percentage designations to their benefit. However, personal information about individual taxpayers who have made the percentage designation is confidential.

After the checks carried out by the State Tax Service on the correctness of the designation, the presence on the List of Beneficiaries, the absence of debts – the beneficiary receives in the account the amounts that have been redirected to him. For 2 years, the beneficiary uses these resources for activities of social importance but also to cover part of its administrative expenditure (according to a formula laid down by law). If the resources have not been used by the beneficiary, they are to be returned to State budget.

The Financial Inspection is responsible for carrying out the control of the use of the sources from the percentage designation. The transparency of beneficiaries’ work is ensured by their obligation to publish activity reports.

Article 152 of the Fiscal Code provides that the beneficiaries of the percentage designation are legally liable for failure to report the use of the amounts obtained as a result of the percentage designation and for the use of those amounts contrary to their intended purpose. Amounts not reported and used contrary to destination shall be returned to the budget. Both the beneficiary organisations and their responsible persons will be accountable. In accordance with point 34 of the Regulation on percentage designation mechanism penalties include an administrative fine, the repayment of the amount used in breach of the rules or failure to report, and the exclusion of organisations from the List of Beneficiaries for two years.

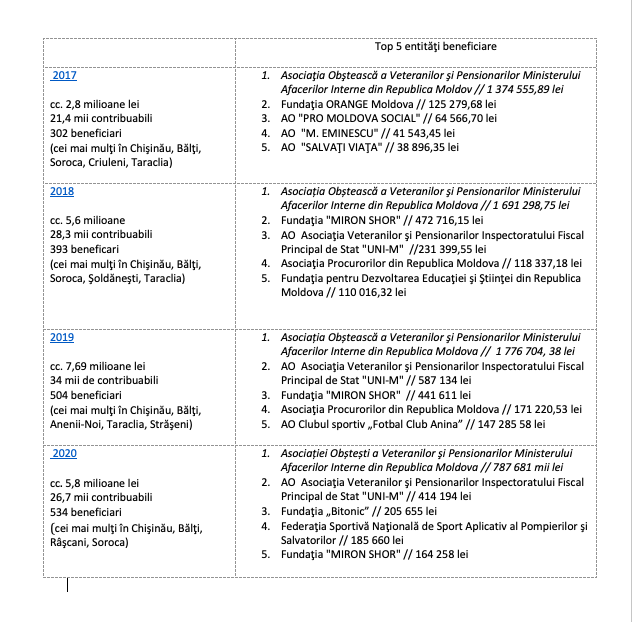

About RON 22 million were designated by obscure and religious associations in 2017-2020

The State Tax Service submits annually relevant data on the amounts allocated, the profile of beneficiaries and statistics on the overall profile of taxpayers participating in this mechanism.

After four years of application of the percentage designation, the activism of professional obese associations is highlighted, in particular the law and force bodies (the top ranks of the list of beneficiaries with the highest amounts received) and sports associations. Religious entities are present in large numbers on the List of Beneficiaries each year, but have so far failed to reach the top five beneficiaries. In the first years of the percentage designation, technical irregularities and lack of awareness of tax arrears by taxpayers were reported – but the mechanism was fine-tuned, including legislative. Non-commercial organisations year-on-year become more active in promoting actions and results to attract 2 %, however redirecting to most of them is modest.

The Obasască Association of Veterans and Pensioners of the Ministry of Internal Affairs of the Republic of Moldova is for four consecutive years the organisation that has received the most resources through percentage designation – cc. RON 5.6 million in 2017-2020. AO Association of Veterans and Pensioners of the Principal State Tax Inspectorate “UNI-M” is the entity present in the third position and second for 3 consecutive years with resources amounting to cc. RON 1.2 million. The Miron Shor Foundation is also on the top five beneficiaries for three consecutive years with cc income. RON 1 million (see below).

Source: bizlaw.md